With many firms evaluating mid-cycle adjustments to pay given the business uncertainty, boards and executive compensation professionals must prepare now to make decisions on short- and long-term incentives. Learn about our framework for an integrated approach.

Business uncertainty continues as we move into the second half of the year. The impact on executive compensation plans will likely be significant, deeming some companies’ previously adopted metrics and goals no longer attainable or rational. Now is the time that compensation committees and their executive compensation professionals need to develop a plan of action for 2020 compensation decisions and 2021 compensation planning. As companies prepare for fall compensation committee meetings, they simply cannot wait any longer to evaluate decisions.

In March and April, as the COVID-19 pandemic hit the United States (U.S.), we recommended companies remain cautious and not react too quickly to revise annual incentives or equity grants until the economic toll of the virus was better known. Now that we are almost six months into dealing with the pandemic, it’s becoming clear that compensation committees will need to use far more discretion than they have in the past. Given scrutiny over executive compensation is far greater in the era of say-on-pay voting than it was a decade ago, compensation committees will want to review performance objectively and rely more on measured judgement than pure discretion to make compensation decisions.

Relevant internal stakeholders — including compensation committees, executives, HR and rewards leaders — should begin the process by thinking through these types of questions:

- How, and how much, should executives and employees be rewarded for results delivered during an unprecedented crisis?

- How do we measure performance when performance measures or goals established early in the year don’t translate to the long-term health of the company given the current environment?

- How do we help compensation committees move from formulaic to measured judgement?

- What should we expect in terms of shareholders’ and proxy advisory firms’ reactions?

To ensure companies are prepared in the coming months to make compensation decisions with measured judgement that withstands intense scrutiny, now is the time to start establishing a process with a solid framework.

A Framework for Making Compensation Decisions

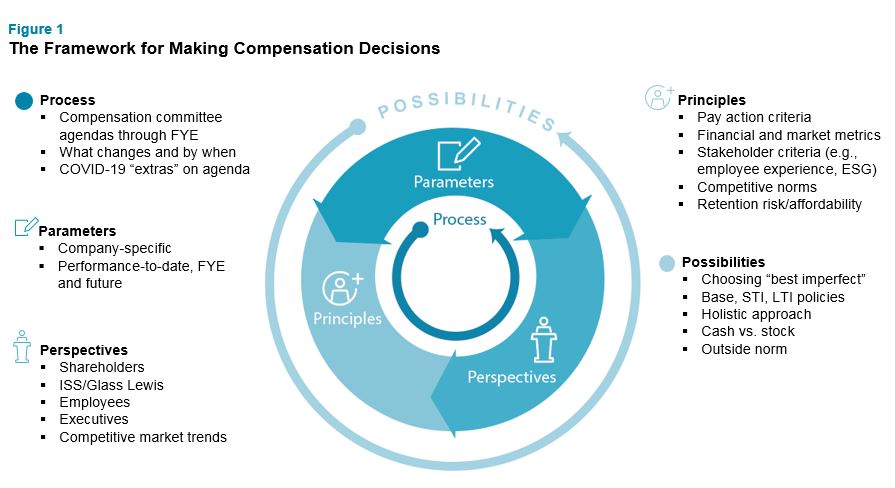

We have developed a framework to help guide companies in making these decisions as they contemplate changes to compensation programs for 2020 and beyond. The five ‘Ps’ of our framework include process, parameters, principles, perspectives and possibilities. Figure 1 highlights the details for each element of the framework.

For the remainder of this article, we’ll explore what each of these framework elements entail.

For the remainder of this article, we’ll explore what each of these framework elements entail.

Framework Component #1: Process

Many compensation committees we have talked to recently believe they will need to use more discretion to make executive pay decisions for 2020 given the timing and severity of the economic impact of the pandemic. Companies making discretionary changes will need to apply a high set of governance standards. Starting a process now will ensure compensation committees have a solid structure to determine how and when measured judgement will be applied and communicated.

As you think through the process of making pay decisions, we recommend following these guidelines:

- Establish a timeline to determine how often the compensation committee needs to meet during the remainder of the year. Evaluate whether additional meetings outside the typical schedule are necessary in order to provide committees with “two bites of the apple” on important issues, such as principles and ultimately choosing between all of the possibilities for annual and long-term compensation actions.

- Draft anticipated meeting agendas that can be modified or added to after each compensation committee meeting.

- Evaluate the work needed to prepare for each meeting and make it most effective for establishing how the committee will gauge performance and determine incentive payouts, if any.

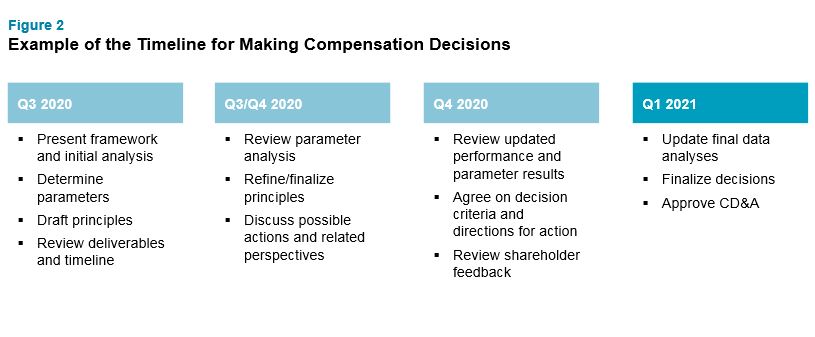

There may be decisions that need to be made along the way to ensure business longevity. However, for incentive plan decisions, we expect that most companies with a calendar year-end will be making those decisions in the first quarter of 2021. Figure 2 outlines a sample timeline for the process to analyze parameters, understand perspectives, determine principles and, ultimately, finalize possibilities into actionable decisions.

The process is key to ensuring the compensation committee has a framework to enable annual compensation decisions, including ones for prior year incentive payouts, base salary increases, current year incentive measures and goals and long-term incentive grants.

Framework Component #2: Parameters

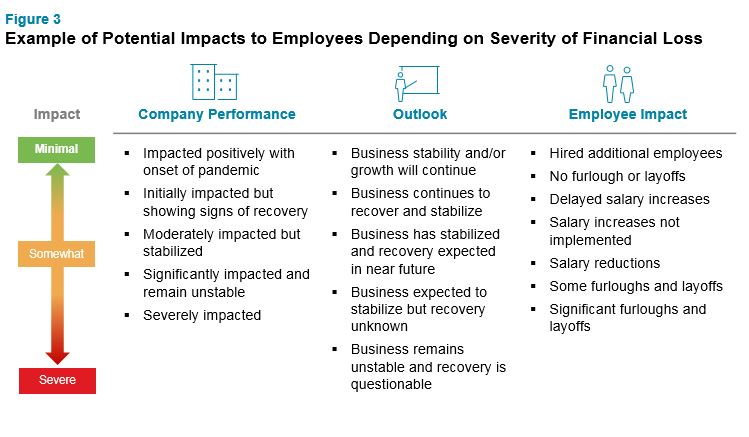

When thinking through whether changes to compensation plans are needed this year, companies should assess how the pandemic has impacted them thus far and best estimate for the remainder of the year. We recommend reviewing three core factors: company performance to-date, outlook for the rest of 2020 and impact to your people. This stage is comparable to medical triage, where there is the need for more immediate action versus further evaluation. Here are some questions to think through in each of the three categories:

Company performance to-date:

- How has the business performed relative to goals set — before the pandemic and historically — at this point in the year?

- What is our cash flow position and profitability?

- What is the current impact to shareholders?

- How are we performing relative to our competitors?

Outlook for future performance:

- What do we expect recovery to look like and how well can we predict the timing and magnitude?

- What are the prospects for our industry and, specifically, direct competitors? Have we positioned ourselves to lead the industry recovery?

- Will there be permanent changes in how we conduct business, and therefore, our profitability?

Impact to employees (e.g., hiring, retention, engagement):

- How have our employees been impacted (e.g., salary reductions, furloughs)?

- What additional employee impacts can we expect, if any?

- How have incentives already been impacted (i.e., what is the realizable value of awards compared to the intended value)?

- Can our incentives drive the behaviors and decision making we need in the new environment?

- What is the likelihood that critical talent will leave and what would be the detriment to the company’s financial and operational wellbeing?

- Will we be able to attract new talent?

The process of asking and answering these questions will help the compensation committee establish parameters for determining possible actions and solutions and, ultimately, deciding which ones are best for the company.

Figure 3 highlights a sample assessment of the magnitude of impact of the pandemic on a company’s business.

Framework Component #3: Principles

The next step in developing a framework is to create guiding principles. These will help answer key philosophical questions, such as: What pay for performance, governance and stakeholder considerations will guide judgment for 2020 compensation actions and 2021 design? What concepts, data and analysis should we consider in making changes to compensation design or level of pay? And, what changes should continue into future years?

Principles will serve as guideposts as the compensation committee begins making decisions regarding current year and/or future pay.

As an example, a compensation committee might consider the following:

- How is our performance relative to peers, historical norms and as measured by the impact of the pandemic (e.g., costs, lost revenue)?

- What is the impact to stakeholders other than shareholders (e.g., customers, communities, suppliers)?

- How are our employees impacted in terms of safety and economic impact (e.g., layoffs, pay changes, changes to work environment due to pandemic)?

- Are we building our foundation for future success?

- Have our peers taken any compensation actions?

- Can we afford the possibilities we are considering?

- What is our risk of losing key talent?

Framework Component #4: Perspectives

There has been minimal guidance from Institutional Shareholder Services (ISS) and Glass Lewis on how they will evaluate pay decisions that differ from the incentive formulas and award opportunities set near the beginning of the year. Both have stated that their evaluation methodologies will hold and exceptions will be reviewed on a case-by-case basis (see our article Proxy Advisors Issue Guidance on Executive Pay and Governance Changes Due to COVID-19 for more information). They have also said that if short- and long-term performance requirements are reduced, so should pay opportunities. Yet, companies may worry about retaining key talent. Doing what is best for the long-term health of the company is equally important for businesses to consider.

Large institutional shareholders have not been any more forthcoming. Every major investor recognizes that the timing and economic impact of the pandemic was large and unexpected, and predicting the remainder of the year (let alone the next three years) will be more difficult than usual. However, it’s also hard to predict how investors will evaluate compensation changes, which makes company disclosure of rationale for any changes more important than ever. Companies may consider whether engaging shareholders and their advisors is prudent to gain support for the changes they are considering.

We always suggest drafting communications for a potential decision even before the final decision is made. Putting the decision down in writing — whether it’s communication to employees, investors or the broader public — makes it easier to assess how the message may be received.

Finally, as we noted in our discussion of principles, an emerging practice is to also consider the impacts of compensation payouts on other stakeholders aside from only investors and their advisors. These include the employees, vendors or suppliers, customers and the community at large.

The perspective of other stakeholders can impact the potential retention risk of a workforce, working relationships with vendors and customers, as well as the company’s reputation in the communities in which they operate. Communicating with other stakeholders to help them understand the business environment and the decisions made will reduce uncertainty and misinformation. Employees’ opinions, in particular, can have a significant impact on attracting, retaining and engaging the company’s workforce. Employees who feel their company is transparent, makes fair decisions and cares about their wellbeing will be less likely to seek other opportunities. Positive opinions by employees also impact the company’s reputation in the community, which can help attract new talent.

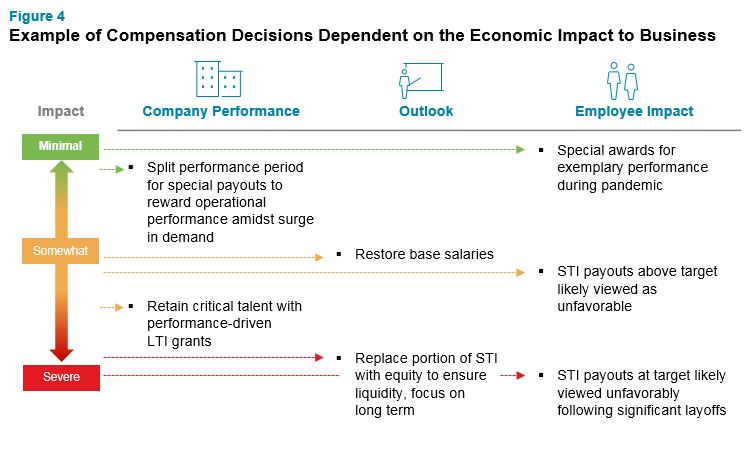

Framework Component #5: Possibilities

The last component of developing a framework for compensation decisions is to consider the possible actions that could unfold from decisions made and why. What are the consequences, intended and unintended, of each possible action?

A myriad of possibilities exists for each component of pay based on the company’s individual situation. Therefore, compensation committees can’t view decision making in a silo for each element of pay — look at the possibilities holistically.

Figure 4 outlines examples of possible compensation decisions based on the company’s assessment of the situation, grounded by the parameters set, perspectives considered and principles established.

While there are no right answers, there is a range of right possibilities for every company. Our framework will help determine the most likely possibilities for each organization so compensation committees can confidently make decisions in an uncertain world.

While there are no right answers, there is a range of right possibilities for every company. Our framework will help determine the most likely possibilities for each organization so compensation committees can confidently make decisions in an uncertain world.

Next Steps

The reality is that compensation committees will need to make decisions with less guidance from governance stakeholders and competitive intelligence than at any other point in the past decade. Decisions will not be easy and documentation supporting how decisions were determined and explained to shareholders and other stakeholders is critical.

There are numerous considerations and follow-up action items even after decisions have been made, including:

- What are the key points of the message when we communicate our decisions?

- How and when will we communicate to impacted employees?

- How will we disclose publicly (e.g., press release, earnings call, company website)?

- Do we need to engage with shareholders and shareholder advisory firms to share our decisions and rationale even before the proxy statement is filed?

We know companies are working hard to adjust to the current environment and lay the foundation to successfully evolve into a “new normal.” Accordingly, we encourage executive compensation professionals and board members to take a thoughtful approach when establishing how they will reward now and in the future for this hard work and the results it will yield.

If you have questions about this topic or would like to learn more, please reach out to one of the authors or write to rewards-solutions@aon.com.

To read more articles on how rewards professionals can respond to the COVID-19 pandemic, please click here.

COVID-19 Disclaimer: This document has been provided as an informational resource for Aon clients and business partners. It is intended to provide general guidance on potential exposures, and is not intended to provide medical advice or address medical concerns or specific risk circumstances. Due to the dynamic nature of infectious diseases, Aon cannot be held liable for the guidance provided. We strongly encourage visitors to seek additional safety, medical and epidemiologic information from credible sources such as the Centers for Disease Control and Prevention and World Health Organization. As regards insurance coverage questions, whether coverage applies or a policy will respond to any risk or circumstance is subject to the specific terms and conditions of the insurance policies and contracts at issue and underwriter determinations.

General Disclaimer: The information contained in this article and the statements expressed herein are of a general nature and not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information and use sources we consider reliable, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without the appropriate professional advice after a thorough examination of the particular situation.

Related Articles