Following a new rule by the SEC last year, companies have begun disclosing details of their human capital management. Using our extensive database, we look at the types of disclosure and provide tips on effectively communicating this topic to stakeholders.

In the early months of disclosing new information about human capital management (HCM), public companies in the United States (U.S.) are focusing primarily on qualitative factors, a variety of topics and communicating more through text vs. visuals. Those are the key findings from our analysis of 101 10-K disclosures that have been filed since the beginning of November when a new SEC rule went into effect.

As more companies file their 10-Ks with this new disclosure requirement, we do expect some of our findings to change given a larger sample size. However, taking an early look at initial disclosures will help companies in preparing their new disclosure for this first year of the requirement.

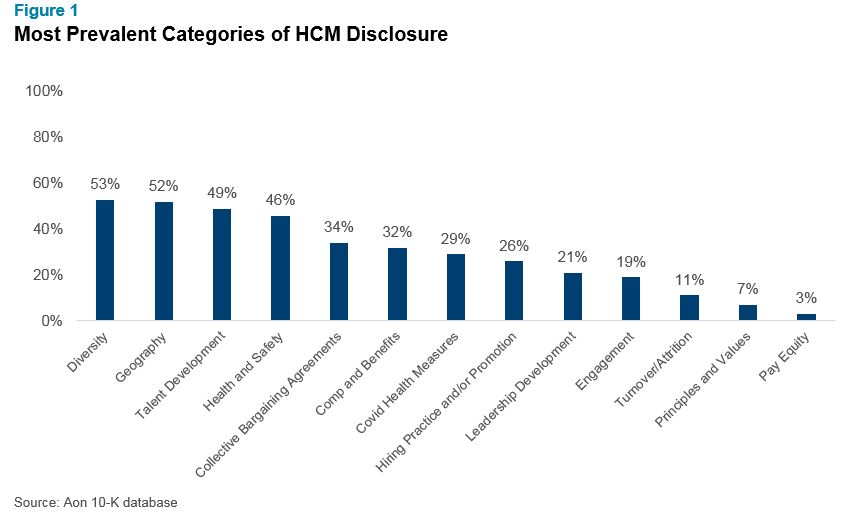

Based on our review, we find HCM disclosure fits primarily into the following 13 categories. Using these categories, we calculated the prevalence of each along with the type of disclosure (qualitative vs. quantitative).

|

|

|

|

|

- Hiring and Promotion Practices

|

|

|

|

- Compensation and Benefits

|

|

|

|

|

|

|

- Collective Bargaining Agreements

|

|

|

|

Key Findings

Information on employee demographics, such as number of employees, geography and diversity had the highest prevalence of both qualitative and quantitative disclosure. On average, companies discussed five categories in their disclosure, including information on the number and geography of employees.

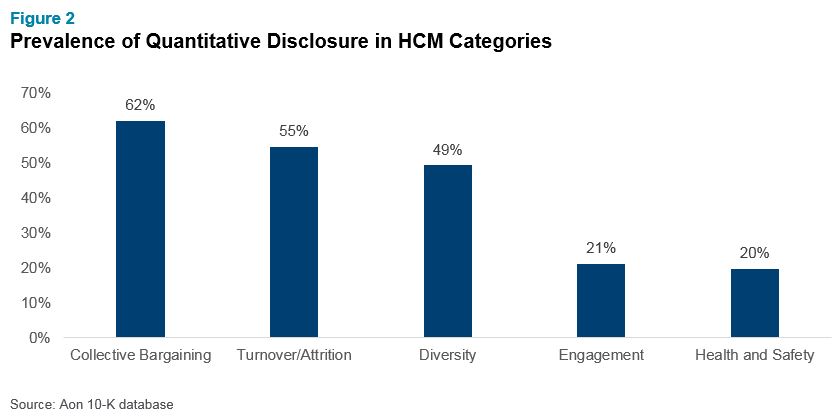

The most commonly discussed categories were disclosures based on employee demographics, such as number and type of employees (employee headcount was an existing requirement for 10-K disclosure), geography and diversity. These categories also had the highest prevalence of quantitative disclosure as shown in Figure 2.

The average number of categories discussed was consistent across industries, with each industry discussing roughly four topics. This includes information on number of employees and geography.

Figure 2 shows the percentage of disclosures that were quanititative (e.g., use of statistics) in nature rather than just qualititative. These five categories had the proportion of quantitative disclosures with collective bargaining and turnover/attrition being the only ones with a majority of quantitative disclosures.

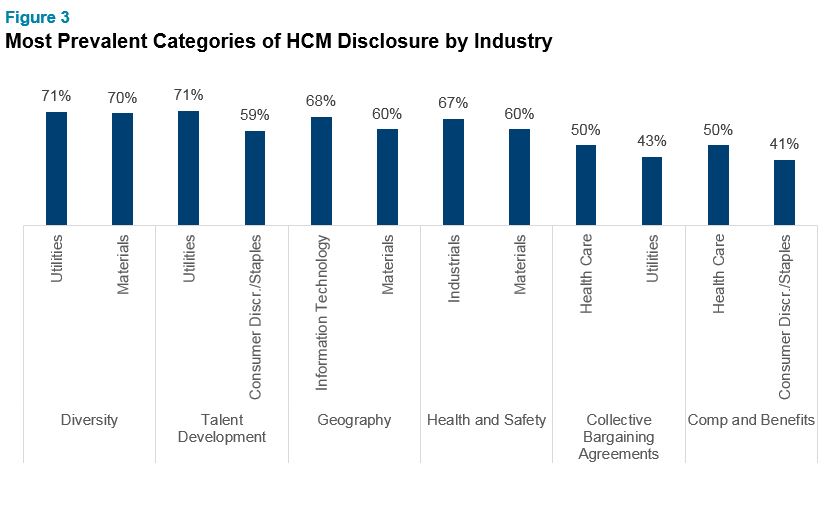

As we look at the categories that were mentioned among industries, it’s no surprise that certain sectors were more likely to provide disclosure more frequently on certain categories. For example, utilities and health care firms were most likely to include disclosure around collective bargaining agreements while industrial firms were more likely to disclose information on health and safety, as shown in Figure 3.

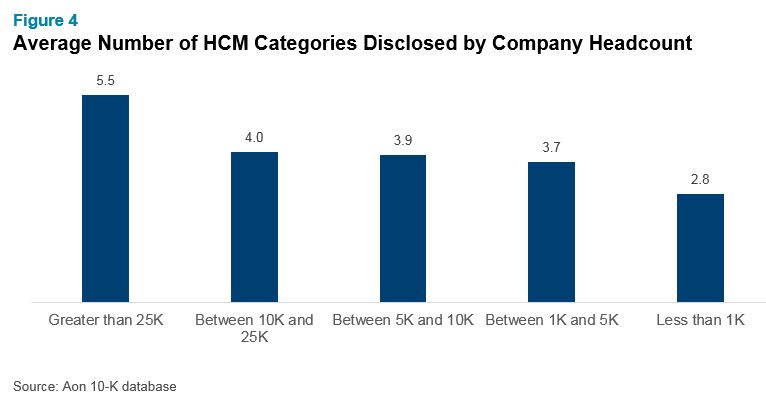

Beyond industry, when we look at company size by headcount, larger firms were more likely to disclose information about a greater number of categories, including diversity, talent development, health and safety, hiring and promotion practices, leadership development and engagement.

Company revenue had a smaller impact on the types and number of disclosures discussed, with larger companies disclosing information on diversity and compensation and benefits slightly more often than the smaller companies.

Most of the disclosures to-date are text heavy with occasional use of graphics or tables to display information. This is reflective of the fact that most disclosures are less quantitative and more qualitative, as HCM is still a nascent area of disclosure. The length of disclosure varies, with the median length approximately 400 words.

As we combed our Aon 10-K database, we found examples of what we believe is effective disclosure in key HCM topics due to their level of detail yet consise language. Here are links to the disclosure for each of the categories:

Next Steps

The most compelling early examples of HCM disclosure, such as the ones above, are organizations that provide clear information that strikes a balance between brevity and detail. We believe stakeholders will be less focused on the length or graphics of the disclosure and more on whether it conveys a compelling message that the company is tracking and monitoring topics of HCM that are relevant to the business and industry. Stakeholders will expect certain types of disclosure — including, in some cases, quantitative measures for particular industries.

It’s also important to keep in mind that while complying with the SEC rule is top-of-mind for issuers, companies shouldn’t ignore the larger picture: Investors, proxy advisors, employees and other key stakeholders are increasingly interested in how companies are managing their human capital. Businesses need a plan for how they will proactively track, measure and communicate HCM over time. We expect disclosures to evolve and become more detailed in the coming years. For more information about steps to take in the longer-term see our article, New Disclosure Rules Bring Increased Transparency to Human Capital Management.

If you have questions about your human capital disclosure and want to speak with a member of our team, please contact one of the authors or write to rewards-solutions@aon.com.

Related Articles