There are many considerations when granting new awards in this environment — changing vehicles, selection of metrics and evaluating performance thresholds. Here’s what companies need to think through when determining when and how to execute upcoming grants.

The economic slowdown is a having a significant impact on company performance across many industries. As more businesses move toward recovery and stabilization (and ultimately to reshaping the future of work), they must rethink and reevaluate total rewards strategies. Companies should take a holistic approach to this opportunity, which is especially true for equity compensation. Equity awards pose unique complexities that cash compensation does not — from accounting and regulatory rules to managing the impact of market volatility.

The first article of our three-part series on addressing employee equity during the COVID-19 pandemic reviewed considerations for your outstanding equity grants. One approach discussed was to address those awards through supplemental grants. However, many companies have concerns about grant sizing if their stock price has fallen, in addition to the potential impact on burn rates, dilution and share pool. In this article, we delve into new grant considerations. These apply to companies that are not on a calendar fiscal year or chose to delay their newest grants to better analyze current market uncertainty or, in some cases, want to simply get a head start on next year.

We should note that these considerations will differ based on industry and the unique circumstances of your organization, including recent performance and expected future performance. It’s important to tailor these elements to your company’s unique situation.

Grant Sizing: Deciding Between Value vs. Shares

With large changes in stock price and increased volatility over a short timeframe, determining the grant size for equity awards is a big area of focus. There are two overall methods used by companies for grant sizing, including granting with a fixed dollar amount or a fixed share amount.

Most companies determine grant sizes by approving a dollar value that is then converted to a number of awards using the stock price, an average price or the accounting fair value. With stock prices decreasing for many industries, this could create “windfalls” with significantly more shares being granted. This scenario is potentially magnified if a firm granted awards earlier in the year prior to stock price decreases, leaving certain employee populations with much larger shares than others. To make sure you determine grant sizes that take into account both competitive levels and share usage, we recommend the following considerations:

- Capping the number of shares at a certain level consistent with 2019 grants (for example, no more than 20% to 30% of shares granted). Paying attention to the share impact on your reserve is important to stay in front of any burn rate or share reserve considerations.

- Factoring in the decrease in value since stock prices began falling across all outstanding grants.

- Considering the likelihood of the stock price rebounding in the near future (if it has not already) and the potential likelihood of future drops during market uncertainty.

- Using an average value, either focusing on the stock price or accounting value, to smooth out some of the volatility. We typically see averaging periods covering approximately one month. (Note: unless it’s necessary for retention, you should avoid the over-increasing of grant numbers at this time and supplement with additional awards later in the year if value does not return due to increases in share price as the business outlook improves).

For companies that base grants on a fixed number of shares, we recommend continuing with this approach for now, even though it will result in lower values granted and reported publicly in the Summary Compensation Table of the proxy statement. If stock value does not return over time (and it has for many industries so far), supplemental grants can be considered later in the year to offset some of the lost value. If employee retention is an immediate concern, increasing grant sizes is reasonable, but it’s important to first consider the impact on the stock price over time and the likelihood of it recovering in the near term.

Rethinking Your Equity Mix

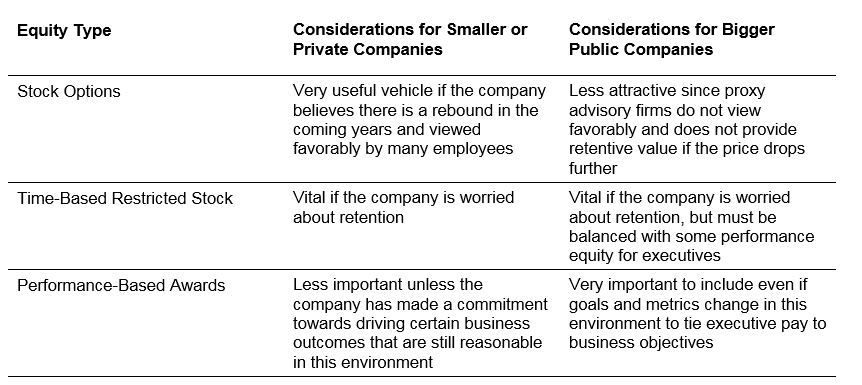

Most companies today use some combination of stock options, time-based restricted stock and performance-based awards. Newly public and emerging growth companies typically use more time-based equity such as stock options and restricted stock. Large public companies typically use more performance-based equity given the guidelines from large institutional shareholders and proxy advisory firms. Contemplating this mix and how it aligns with your business objectives in this environment is vital. The table below highlights some key considerations.

Considerations for Stock Options

Stock options can be an attractive vehicle, particularly if you feel your stock price is artificially low and will bounce back. This could create a very sizeable return for option holders depending on the level of stock price recovery. We recommend a more broad-based approach to options. If everyone has access to stock options, this vehicle could be an attractive method of retaining employees through this volatile timeframe, especially if the company’s value has been artificially lowered. If stock options are limited in the organization or options have not performed well over recent years, consider the message it sends to the broad population who may be feeling the impact of the economic environment. Furthermore, if your industry was completely upended by the pandemic, the use of options may not be appropriate going forward, as they will have little perceived value by your participants. These awards, in general, should fall within your grant policy and be carefully reviewed to avoid any “spring-loading” perception (i.e., granting options at a time that follows a positive news event).

Additionally, you should also understand the increased dilutive impact stock options will have granting at a lower stock price. For most companies, one share is equal to two to four stock options, allowing for the use of significantly more shares through this method. Furthermore, given the mechanics of options, it’s worth thinking about the likelihood of a bounce-back or further decreases in value and the impact on retention, as that could dictate whether the newest option grants are worth anything in the coming months or add to your underwater equity.

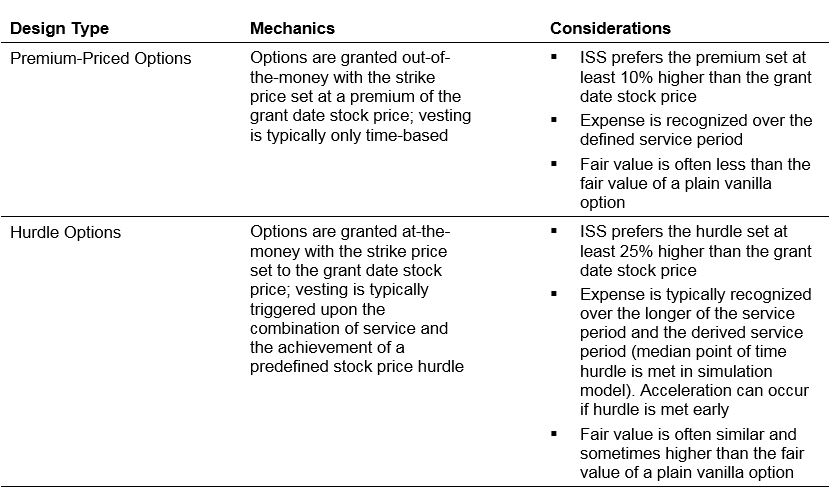

Finally, for companies contemplating supplemental awards that are in addition to the normally occurring awards, the use of performance criteria will help the rationale for this grant resonate externally. The two methods to use for stock options to make them performance based under ISS’ criteria are summarized below. Please note that Aon prefers the use of premium-priced options since the required performance level is not as high in the eyes of ISS, the company better controls the timing of expense, and the cost of the award tends to be lower.

Considerations for Time-Based Restricted Stock or Units

Given the retentive value of these awards and the ability to hold value even in down markets, this is a commonly used instrument, particularly for companies granting equity broadly. If your focus is retention during this time, no other vehicle will do a better job of addressing that concern than time-based restricted stock. However, at the executive level, performance equity will be expected even if goals change drastically as a result of the pandemic, so significant use of time-based restricted stock at the executive level should come with a very clear rationale as to why it’s needed.

Considerations for Performance-Based Awards

Performance-based equity is particularly important for supplemental or retention grants for executives. With sensitivity from investors and proxy advisory firms to these types of grants, using performance-based equity will bring more perceived alignment between executives and shareholder value. With that said, the idea of setting goals in this environment may seem overwhelming. Companies drastically impacted by the current economic situation may need to revise goals or metrics.

Evaluating historical performance in various economic environments, how peers have recently performed, as well as data and projections can provide a baseline — and help with public disclosure. Any changes in your design for new grants should be clearly disclosed with a supporting rationale.

If you haven’t already, it’s a good time to think about adding relative metrics, particularly relative total shareholder return (TSR). The use of this metric helps to address concerns around setting realistic long-term goals with other operating metrics. It is also designed to be fair and effective in all economic environments. Even when the market is down, if you outperform your peers and are a superior investment for shareholders over that timeframe, payouts can be justified.

Another measure to consider going forward is incorporating environmental, social and governance (ESG) factors into your long-term incentive plans — an impactful step to take in a normal environment that is potentially even more impactful now, in light of the health and safety effects of the COVID-19 pandemic.

Delivering Cash Plans in Equity

A broader consideration for companies is assessing whether the use of cash or equity will be more valued by employees and how these programs are viewed by shareholders at this time. For companies focused on preserving cash resources, equity could be very useful since it comes with a non-cash charge and the expense can be recognized over the vesting period. Additionally, with a long-term view, we’ve seen equity have a much higher return to employees than cash, landing on average 30% to 50% higher than the cost realized by the company to issue those equity awards. It may not feel like equity is effective right now with the market volatility, but the long-term return tends to be significant.

With that in mind, there are a few paths companies could explore to deliver more compensation via equity. It’s important to note that these programs will increase the use of shares, so you’ll need to analyze share usage and dilution.

- Develop a program where employees can elect to receive a percentage of salary in stock that could vest immediately or over time.

- Create a market where employees buy shares of the company at the market price or a discounted price, which creates a cash inflow for companies as employees buy shares. For companies that maintain Employee Stock Purchase Plans (ESPPs), the flexibility to leverage this program may already exist.

- Set a limit in your short-term incentive plan where any value above threshold or target is delivered in stock. Shares used in this manner do not count towards your burn rate and the cost of those shares can be spread out over an extended period if their vesting requires additional service.

Overall, the use of equity can help companies manage compensation and cash flow effectively, but it’s important to recognize that expense does not necessarily decrease with these programs. There are certainly ways to structure equity awards to save cost but, in some cases, the expense is comparable. However, if your concern is focused on preserving cash resources, expanding your use of equity could have a very significant impact.

Next Steps

There are many considerations when it comes to planning and granting new awards in this environment. You may need to change vehicles, explore new metrics or evaluate performance thresholds. There may even be a need to increase grant sizes with future awards to offset some of the “lost” value associated with many outstanding awards today. As you navigate the future and set course on your next grants, make sure to pay attention to the following:

- The vehicle types that best fit your needs going forward

- Your current evaluation process for metric selection and goal setting

- The inclusion of market-based metrics to best align with shareholders and avoid problems with long-term goal setting

- The accounting implications of any changes in design or structure

- The dilution impact of future grants and how that may change the frequency at which you request additional shares

- The early disclosure of rationales for any changes you make; scrutiny of compensation plans will only increase during this time, so be transparent and fair in your reasoning

Stay tuned for our next and final installment in our series, where we will discuss developing a communications strategy around your equity plans.

For questions about any of the issues discussed in this article, please reach out to one of the authors or write to rewards-solutions@aon.com.

To read more articles on how rewards professionals can respond to the COVID-19 pandemic, please click here.

COVID-19 Disclaimer: This document has been provided as an informational resource for Aon clients and business partners. It is intended to provide general guidance on potential exposures, and is not intended to provide medical advice or address medical concerns or specific risk circumstances. Due to the dynamic nature of infectious diseases, Aon cannot be held liable for the guidance provided. We strongly encourage visitors to seek additional safety, medical and epidemiologic information from credible sources such as the Centers for Disease Control and Prevention and World Health Organization. As regards insurance coverage questions, whether coverage applies or a policy will respond to any risk or circumstance is subject to the specific terms and conditions of the insurance policies and contracts at issue and underwriter determinations.

General Disclaimer: The information contained in this article and the statements expressed herein are of a general nature and not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information and use sources we consider reliable, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without the appropriate professional advice after a thorough examination of the particular situation.

Related Articles