A new SEC rule requires U.S. public companies to disclose factors that are material to driving and impacting human capital. We recommend firms define an intentional human capital management strategy that is clear and measurable before communicating outward.

There is growing recognition that a company’s greatest asset is their people — and events like the COVID-19 pandemic and widespread protests for greater social justice are catalysts for driving people risks to the forefront. Transparency around how companies manage their human capital is of particular interest to stakeholders like investors, regulators, proxy advisors and employees.

At its foundation, human capital management (HCM) is the practice of investing in and developing employees to enhance business value as part of a broader environmental, social and governance (ESG) strategy. Large institutional investors like BlackRock and State Street Global Advisors have been pressuring public companies for the past few years to expand disclosure and engagement on HCM. In light of the increased focus, some compensation committees, especially at larger companies, have revised their charters to add oversight of “human capital” or “people management” and have expanded the name of the committee to signify its importance. However, formal reporting on HCM activities within ESG reporting has historically not been as robust as desired by investors, proxy advisors and other stakeholders.

Amid growing pressure from these groups, the SEC approved a new rule that requires companies to disclose quantitative and qualitative factors material to driving and impacting human capital as part of its business description in its Form 10-K. The SEC rule is “principles based,” meaning the SEC deliberately did not define HCM or provide a specific list of topics or quantifiable metrics that must be disclosed. Without prescriptive guidance from the SEC, and a lack of existing disclosure examples, many of our clients are asking us where they should begin.

Look Inward Before Communicating Outward

While numerous large-cap companies already report on various HCM-related activities, such disclosure is the exception rather than the norm in the broader marketplace. And even among those companies that provide a level of HCM reporting, it is not uniform across companies or industries. As such, we believe that most companies should view this new SEC rule as an opportunity to look inward to define their HCM philosophy. As part of setting this strategy, it is crucial to identify key, measurable metrics that comprise a holistic approach. This will begin to pave a path forward, as we anticipate that the new disclosure rule and companies’ interpretations of it will evolve over time, leading to even more transparency.

We recommend companies approach this new disclosure in two phases: first, reacting to the HCM disclosure requirements, and then proactively tracking and communicating key metrics. Let’s discuss the steps involved in each of these phases.

Phase 1: Reacting to HCM Disclosure Requirements

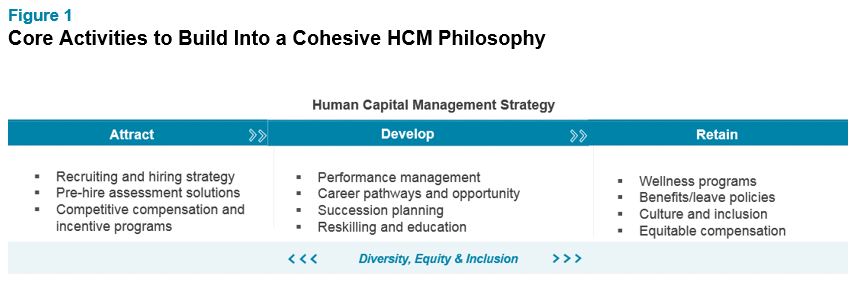

The first step is to take stock of your current human capital efforts as they relate to attracting, developing and retaining employees, while being mindful of how inclusion and diversity might affect and drive strategy in each of those categories. Across most organizations — regardless of how far along a company is in its HCM journey — programs are in place that focus on elements of attracting, developing and retaining talent (as outlined in Figure 1). But often these efforts are managed and tracked independently of one another and lack a cohesive story. Companies can leverage this inventory of programs and practices, together with management objectives, to define an HCM philosophy.

The next step is to get organized for the current year disclosure. Determine if there are programs and practices that you can immediately report on — at least qualitatively. Many companies are unlikely to report on quantitative metrics for fiscal year 2020, particularly in the Form 10-K, as this disclosure has a higher standard of liability and is subject to disclosure controls and procedures that are certified by the CEO and CFO and then approved by the board.

Phase 2: Proactively Track, Measure and Communicate — Then Repeat

Starting in 2021, companies should begin evaluating whether it is time to enhance HCM practices and reporting by implementing the following steps:

- Step 1: Identify quantifiable metrics you want to start measuring that tie back to your HCM strategy and implement appropriate disclosure controls and procedures so that you can report on them in the future.

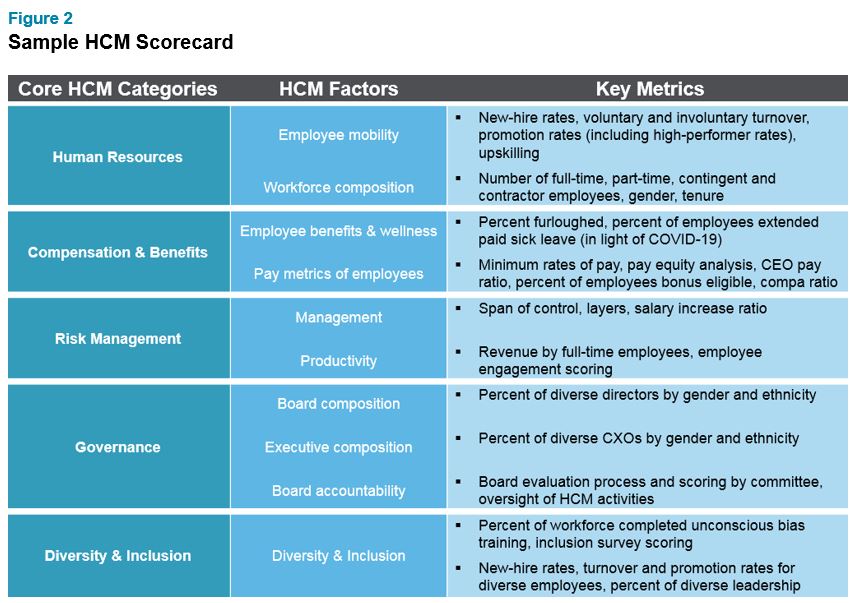

- Step 2: Identify any opportunities or gaps in your HCM strategy relative to your industry peers by using relevant market data to benchmark against internal metrics. If you are a participant in Aon’s rewards surveys, we can define and standardize key metrics for your firm and provide relevant benchmarks. Figure 2 shows a sample HCM scorecard.

- Step 3: Implement programs and practices to drive progress toward HCM goals. Once gaps or opportunities in your HCM approach have been identified, it is important to take a measured approach to improving metrics. Change takes time and you need to build flexibility into programs, recognizing that internal and external variables can alter company goals and focus over time.

- Step 4: Communicate to stakeholders through various methods, including internal employee-centric communication. Once progress is communicated, companies should continue to be vigilant by identifying any new gaps, tracking ongoing progress and staying on top of evolving disclosure requirements.

Next Steps

Rather than looking at the SEC rule as a check-the-box compliance activity, we view it as a reflection of the collective belief in the market of the value of well-managed human capital. Companies have an opportunity to differentiate themselves by defining their HCM philosophy and then translating that into measurements to help them communicate with external and internal stakeholders on this topic.

To learn more about how we help organizations manage their human capital and determine the relevant measurements for reporting, please reach out to one of the authors or write to rewards-solutions@aon.com.

Related Articles