The proposed rules would require additional disclosure from proxy advisory firms and allow companies to preview the proxy recommendations in advance as well as provide a rebuttal.

The Securities and Exchange Commission (SEC) has continued its focus this year on the activities and influence that proxy advisory firms have on the proxy voting process. On November 5, 2019, the SEC approved, by a 3-2 party-line vote, proposed rules to regulate proxy advisory firms. These rules are subject to a 60-day public comment period and, if finalized, would take effect after a one-year transition period — most likely for the 2021 proxy season.

The proposed rules are the most recent in a busy year for the SEC when it comes to proxy advisory firms. In August, the SEC released two sets of guidance (each approved by a party-line vote). One set of guidance provides clarity to the SEC’s interpretation of the proxy solicitation rules as they relate to the voting guidance provided by proxy advisory firms and the other focuses on the responsibilities of investment advisers utilizing proxy advisory firms’ vote recommendations. In response to the guidance, in late October ISS filed a complaint against the SEC in the U.S. District Court for the District of Columbia, on procedural and substantive grounds.

The rules, as proposed, would significantly impact proxy advisors’ reports and recommendations in two significant ways:

- Disclosure of conflicts of interest, and

- Mandatory review, comment, and publication notice to issuers.

Conflicts of Interest

The proposed rules begin with the premise that proxy voting advice is a proxy solicitation, subject to the proxy solicitation rules (including the filing requirements) unless an exemption exists. The availability of these exemptions is critical to the proxy firms’ business, as they would not be able to charge fees to their clients if required to publicly file their vote recommendations.

The proposed rules would condition the exemptions most commonly used by the proxy firms by requiring that they disclose:

- Any material interests, direct or indirect, of the proxy voting advice business (or its affiliates) in the matter or parties for which it is providing the advice;

- Any material transaction or relationship between the proxy voting advice business (or its affiliates) and (i) the issuer (or any of the issuer’s affiliates), (ii) another soliciting person (or its affiliates), or (iii) a shareholder proponent (or its affiliates), in connection with the matter covered by the proxy voting advice;

- Any other information regarding the interest, transaction or relationship of the proxy voting advice business (or its affiliate) that is material to assessing the objectivity of the proxy voting advice in light of particular interest, transaction or relationship; and

- Any policies and procedures used to identify, as well as the steps taken to address, any material conflicts of interest arising from such interest, transaction or relationship.

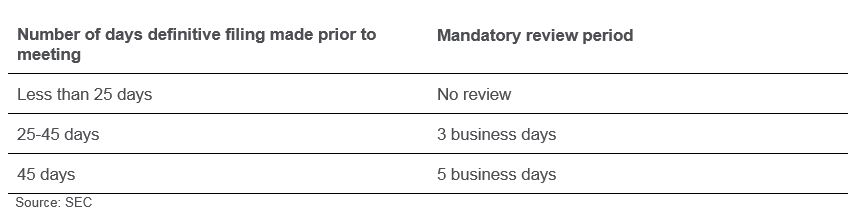

Mandatory Review

The proposed rules would require that proxy advisory firms provide issuers, and certain other soliciting persons covered by proxy voting advice, a limited amount of time to review and provide feedback before distributing to clients — who are primarily institutional investors. The proposed rules would allow a proxy advisory firm to require that the information be kept confidential as a condition of receiving the proxy voting advice. The length of time provided would depend on how far in advance of the shareholder meeting the company has filed its definitive proxy statement. The review periods are as follows:

The SEC noted that most companies file their proxy statements between 35-40 days prior to their meetings. Given this average, the majority of companies would receive three to five days advance notice to review proxy advisory firms’ recommendations, which allows them to clarify or correct errors, as well as prepare a response to their shareholders.

Publication Notice

In addition to the review and feedback period, proxy advisory firms would be required to provide issuers and certain other soliciting persons with a final notice of voting advice at least two business days prior to publication of its voting report to clients. This would give companies the opportunity to determine the extent to which the proxy voting advice has changed from the draft advice, including whether the proxy firm made any revisions due to feedback from the issuer. This notice must be provided, whether or not registrants added comments to the version of proxy voting advice they received during the review and feedback period.

Opportunity to Respond

Under the proposed rules, issuers and certain other soliciting persons would also have the option to request that proxy advisory firms include in their voting advice a hyperlink to an issuer’s written statement about its own views on the advice. The ability to include a hyperlink response in the proxy voting advice ensures that alternative points of view are available to investors, the SEC says.

Next Steps

We will continue to monitor these proposed rules and provide additional analysis as relevant updates occur. In the meantime, if you have questions about future SEC plans or other corporate governance-related matters and want speak with a member of our rewards consulting group, please write to rewards-solutions@aon.com.

Related Articles