Issuers that received declining say-on-pay support and/or triggered a Board Responsiveness Policy from a proxy advisory firm will need to take a multi-step approach for 2020 planning.

As we head into the fall compensation committee planning months, it is helpful to review what occurred in the 2019 proxy season and apply those lessons learned in preparation for the next one. One of the most closely watched proxy items in the United States is the annual say-on-pay vote. Continuing the trend from the 2018 proxy season, many industries experienced an increase in the percentage of companies where support fell below the key threshold for proxy advisory firms (70% for ISS and 80% for Glass Lewis) — meaning that boards should be engaging with shareholders in the off season and assessing whether further action to modify pay programs is warranted.

In this article, we’ll dive into specific voting results by industry, provide insights around why support has declined and advice for issuers as we head into 2020 proxy season planning.

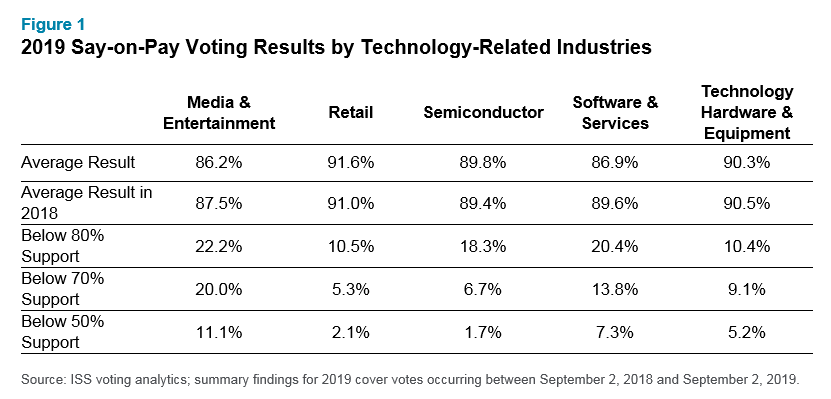

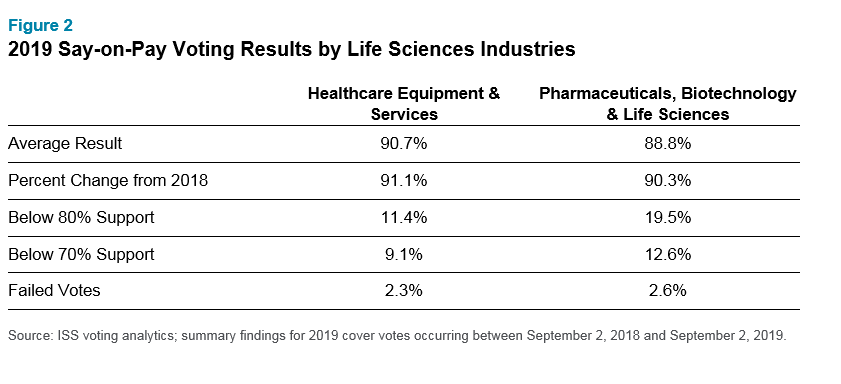

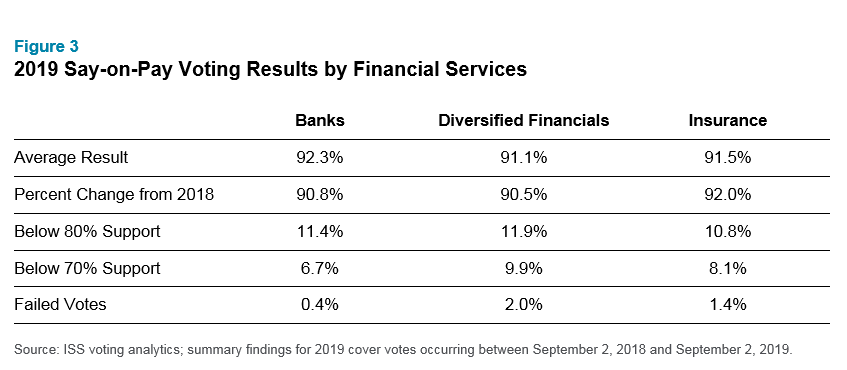

Average Say-on-Pay Support by Industry

The average vote result among all Russell 3000 companies remained nearly static in 2019 at 90.6% compared to 90.7% in 2018. While outright failures also remained relatively flat at 2.3% in 2019 vs. 2.4% in 2018, there has been an uptick in the number of companies triggering the ISS and Glass Lewis Board Responsiveness Policies. This policy is triggered for ISS when companies receive less than 70% support; for Glass Lewis the threshold is less than 80% support. At the same time, ISS and Glass Lewis have remained consistent year-over-year in the percentage of negative say-on-pay voting recommendations they provide. Industries that saw an increase in companies falling under one or both proxy firms’ Board Responsiveness Policies include healthcare equipment and services, insurance, life sciences, retail, semiconductors, software and services, and technology hardware.

Certain industries saw declining year-over-year say-on-pay results from 2018 to 2019, including healthcare equipment and services, insurance, life sciences, media and entertainment, software and services, and technology hardware. These results signal that investors are increasingly unwilling to provide corporate issuers the benefit of the doubt in a continued trend of escalating CEO pay levels and more volatile stock prices. But other industries — such as banking, diversified financials and retail — saw improved year-over-year say-on-pay results.

Key Drivers of Declining Say-on-Pay Results

While pay-for-performance related concerns continue to be the key driver of against recommendations from proxy advisory firms and the reason institutional shareholders vote against pay plans, there are other contributing factors. These include:

- Inadequate disclosure around short- and long-term incentive goals, as well as a lack of clarity on the equity grant sizing process

- Lowered incentive goals without adequate rationale

- Increased target incentive opportunities when underperforming relative to the industry

- Large one-off grants without sufficient rationale and/or risk-mitigating design features

- Above median benchmarking (especially when using outsized peers)

Companies that failed to obtain majority approval in 2019 or triggered a Board Responsiveness Policy will be expected to disclose in 2020 that they engaged with shareholders following the last annual shareholders’ meeting to understand their concerns and took some action to address those concerns. Absent such action, companies face possible negative vote recommendations for both say-on-pay and the re-election of compensation committee members. Even if a company is technically above the proxy advisory firm voting thresholds for these policies, it is good practice to engage with investors if your say-on-pay results have gone down from the prior year as it indicates increased investor dissatisfaction with some element of your pay program.

Next Steps

There is still time for companies to take action for the 2020 proxy season by following a multi-step process.

- Assess prior year exposure and take action if necessary: If you saw declining vote results and/or triggered a Board Responsiveness Policy from a proxy advisory firm, a shareholder engagement effort and committee action in response to shareholder concerns are necessary to avoid continued issues in 2020. Committee action could be the adoption of various compensation governance best practices or maybe even be enhanced disclosure and transparency on the executive compensation planning process.

- Re-evaluate your disclosure: Companies and their compensation committees spend a lot of time and effort on thoughtfully crafting pay strategies. However, it is not uncommon for those efforts not to come through in narrative disclosure. Consider reviewing your prior messaging to see if there is a better way to communicate your story more effectively for the 2020 proxy season. The use of easy-to-read graphics can be especially helpful in communicating certain processes or pay level decisions. For more information about alternative and potentially effective pay disclosure, see our recent article Take Your Compensation Disclosure to the Next Level by Reporting Realizable Pay.

- Understand your current year exposure: In addition to looking back at exposure from prior season voting results, companies should also be looking at current fiscal year decisions (including new hires, leadership transitions and special one-off compensation arrangements) and pay-for-performance scoring to determine the level of likely proxy advisor and investor scrutiny. If the situation appears controversial, the Fall months are a good time to craft talking points for shareholder engagement and to enhance the CD&A story.

If you have questions about preparing for the 2020 proxy season and want to speak with one of our experts, please write to rewards-solutions@aon.com.

Related Articles