Ensure your sales compensation programs are aligned for success by avoiding these common mistakes.

Sales compensation programs remain pivotal to the success of many sales focused organizations, helping to align business interests to those of the sales staff and sales team. It is therefore no surprise that firms across most industry segments utilize some form of a compensation plan.

Their ubiquitous and industry agnostic nature, however, does not always guarantee success. If designed and/or implemented incorrectly, sales compensation structures can cause more harm than good. For this reason, many organizations are taking a hard look at their existing plans, finding ways to optimize them and ensure that they remain aligned to business goals.

How can firms avoid common pitfalls plaguing their sales compensation structures? In this article, we highlight the top reasons your plan may not be working.

1. Overly complex

The success of any variable pay program hinges on the participants’ abilities to understand how their actions influence end outcomes. This is particularly true for sales compensation plans, which are often triggered by individual performance.

Even the best designed plans fail if they are not well understood or are innately complex. The complexity of plans can stem from two sources:

- Plan mechanics: Plans with multiple layers of thresholds, multipliers, caps, and quotas are unlikely to enthuse individual sales contributors. Such plans pose the risk of participant distrust, potentially leading to wrong perceptions and the view that the organization is unwilling to release incentive payouts under the guise of an overly complicated structure.

- Plan duplication: As businesses evolve over time with new products, variants, and markets, there is a tendency to create new plan structures, often with a different set of documentation. This leads to inconsistencies and creates a plethora of plans, when in fact, the simple solution in such cases is to vary the targets.

2. Gaming

Plan design should incorporate suitable checks and balances to ensure that there are no opportunities for gaming or collusion. Ill-conceived plans often witness gaming through the timing of a sale, which is also an important parameter to consider for sales credit. Are incentives due for booking the sale, or against the execution of the contract and payment?

The inability to accurately tag production to an individual can create opportunities for collusion and result in increased cost of incentives for similar production levels. Worse still, it can elicit inappropriate participant behavior. Plan mechanics should also permit a reasonable upside for higher production levels, which depends upon the perceived difficulty of those levels. Failure to do so could increase the chances of sandbagging—when participants operate in ‘cruise mode,’ anticipating the incentive as guaranteed.

3. Not involving the business

Not involving the business Sales compensation plans often depict the proverbial ‘tug of war’ between the HR function and the business. However, exclusively relying on the business can result in plan structures that are not compatible with the firm’s overall pay philosophy. On the other hand, excluding business/sales functions from the decision making process can jeopardize plan design due to inappropriate measures and target setting. This also carries the risk of not accounting for the sales process and business model in the mechanics of the plan.

Best practice suggests that businesses follow a partnership approach through the creation of Incentive Oversight Committees. By doing so, firms will receive participation from a multitude of functions—HR, finance, business, and risk. The core objective is around effective design, implementation, and governance of sales incentive architecture.

However, sales plan governance often does not get the attention it deserves. Poor governance can lead to many issues including financial losses, opportunities for fraud, regulatory fines, and more.

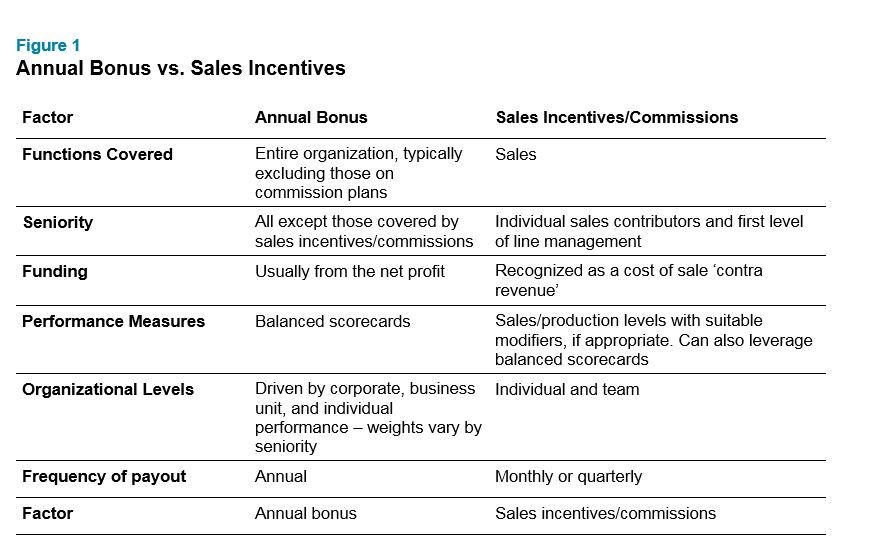

4. Confusing bonus with incentives/commissions

While the terminology is often used interchangeably, there are clear differences between an annual bonus plan and a sales incentive/commission architecture.

The following table illustrates the key differences between the two. Please note that while this example is reflective of typical plan structures, other variations and combinations are possible.

The above differences are identified to help recognize the correct plan choice based on various parameters.

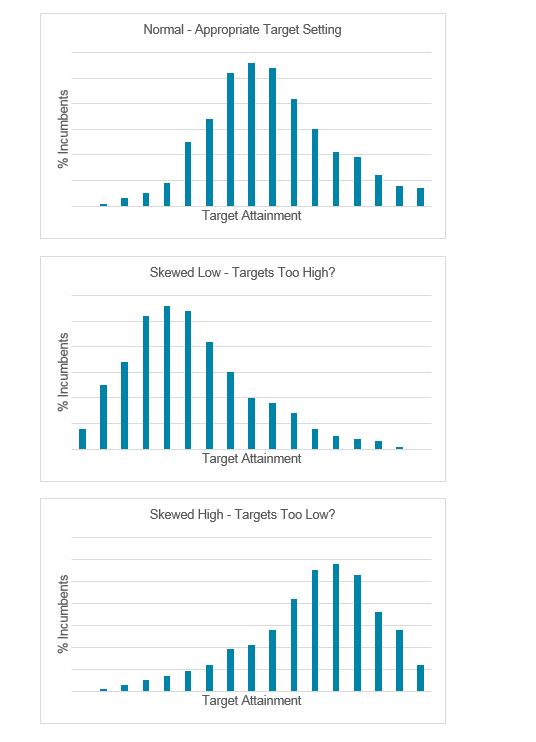

5. Target setting

Target setting should include different parameters—market opportunity, competition, product portfolio, sales team headcount, administrative support, etc.

However, firms must ensure that the biggest driver of target setting is past performance and payout distributions. The old adage, ‘history repeats itself’ is true, especially when it comes to performance distributions. Organizations should continually review past patterns to keep their target settings up to date.

Additionally, thresholds should ideally reflect the probability of 85% - 90% of the population achieving desired results, while targets should reflect a corresponding probability of 50% - 60%.

The charts below show different skews reflective of the difficulties of the targets set. In other words, each figure reflects the likely performance distribution when the targets are set too low, just right, and too high.

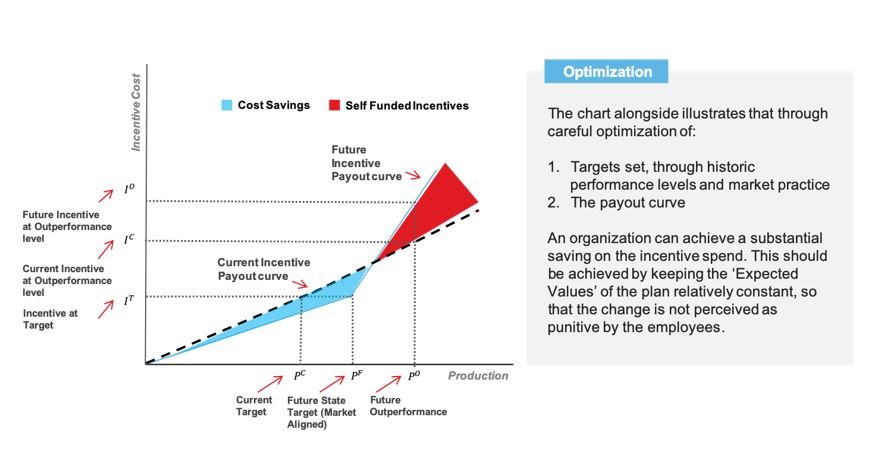

6. Inappropriate allocations

A well-designed sales incentive program allows participants to earn incentives at the appropriate difficulty level. For an effective program, the right incentive should be allocated to high performers. An overly socialistic approach to commission structures is doomed to fail, as it is unlikely to elicit the right levels of motivation from top talent. In many organizations, a significant portion of the overall production is delivered by the top 30-40%. In such cases, all efforts should be made to redirect the allocation towards higher production levels.

Carefully calibrated allocations can result in substantial reductions in the overall cost of sales, while improving participant motivation levels. The image below describes this in more detail.

7. Inappropriate measures

Performance measures are pivotal to the success of any sales compensation program. At the heart of this decision-making process are two key factors, which are often discussed in classic academic literature:

- Line of sight: Do the participants have the ability to impact the desired outcome?

- Alignment: Does the achievement of desired objectives help the organization reach intended strategy? For a firm trying to gain market share, incentivizing sales employees on margins may not help.

It is also important to assess whether the incentive plans should be triggered based on individual or team performance. In situations where individual sales delivery is not possible without the active support of colleagues from both inside and outside the sales function, team-based sales plans are usually more appropriate. In such cases, sharing may be allocated in one of two ways:

- Sales incentive pool determined centrally based on production achieved / individual allocations made based on pre-set criteria.

- Sales incentives determined at an individual level based on individual production achieved; however, a set percentage is carved out for another team.

Another aspect to consider is the role of discretion or subjectivity in sales plans. Although purely discretionary sales plans are rare, elements of discretion may arise from discretionary elements in scorecard driven sales plans or from any docking criteria applied.

8. Inappropriate participation

It is good practice to restrict participation in sales compensation plans from employees with a direct line of sight to sales. In most cases, this includes individual sales contributors and the first level of line management within the sales function.

Many organizations make the mistake of democratizing the setup with a wide base of participation that extends up to the most senior levels within the organization. This approach is flawed for two reasons—first, it dilutes the attention and focus of the plan away from the intended target group of the individual sales contributors; and second, it often has the tendency to create distorted behaviors, causing senior managers to focus on short-term sales at the expense of the organization’s long-term game plan.

While there are situations that require participation at the most senior levels, it is usually an exception rather than the norm. In most cases, we recommend that firms incentivize their senior management through annual bonus plans in place of sales incentives.

Next Steps

Sales compensation plans are among the most widely used rewards structures. They provide a clear, direct linkage between production and incentives, and thus, if structured appropriately, can help orient employee behaviors in the right direction. Well-designed sales plans are often self-funded, helping to perfectly align the interests of the sales representatives with those of the shareholders and management.

Unfortunately, it is also very easy for these plans to go awry. The next time you review your firm’s sales compensation programs, be sure to keep these common pitfalls in mind to derive the best results.

To learn more about sales compensation plans and ensure your firm is on track for success, please write to rewards-solutions@aon.com.

Related Articles