This is Part II in Incentive-based Compensation Arrangements: A Summary of Dodd-Frank Section 956.

After five years, the interagency task force has re-proposed Section 956 of Dodd-Frank.

As of this writing each regulatory body has issued its proposed rule, with each agency having some variances in their published rules; however, it is yet to be published in the Federal Register. The formal comment period ends on July 22, 2016.

Update to earlier summary

The update provides an executive summary of critical strategic issues, a deeper dive on tactical implementation issues, and definitional clarity on key topics. McLagan has been in communication with members of several regulatory bodies and based upon those communications developed our perspective for this alert. While we believe the substance of each agency's proposal is aligned, we acknowledge the potential for nuances as the proposals range from approximately 300 - 700 pages in length, depending on the agency.

Proposal in concept

-

Three levels of classification beginning at $1 billion and resetting at $50 billion and $250 billion in assets with regulators reserving the right to subject firms to the more stringent requirements of a larger institution

-

Generally, subsidiary organizations are subject to the requirements of the parent company except in the case of the SEC's proposed rules which indicates that subsidiary institutions are subject to rules based upon the asset size of the broker-dealer

-

All incentive eligible employees are covered by the rules with two primary employee classifications that carry specific compensation requirements: Senior Executive Officers (SEO) and Significant Risk Takers (SRT)

-

For firms $50 billion and larger: all incentive compensation for SEOs and SRTs includes deferrals and 7 year clawbacks

-

All covered institutions have a 7 year record keeping requirement; records will need to be made available to regulators upon request

-

All incentive compensation must be balanced, have effective controls, and board oversight

-

Incentive compensation plans must be in compliance beginning the first calendar quarter after an 18 month period from when the rules are finalized; generally thought of as 2019 for annual based plans

Executive summary of key issues

The following provides a summary of key issues / unintended consequences within the proposal. These issues are intended to highlight areas which should receive proper attention and potential comment by July 22, 2016. Each financial institution should determine how they would want to comment: individually, collectively, or both.

-

Relative compensation test: The present test provides for classification as a SRT if the covered persons are in the top 5% (Level 1 firms) or top 2% (Level 2 firms) of all covered employees. This is one way to determine who is a "highly compensated employee" and, therefore, should be subject to the defined deferral requirements. An important question is whether an absolute compensation level (e.g., employees who make $1 million or more; indexed for inflation) might be more appropriate.

-

Exposure test: The present test requires employees who have the ability to commit 0.5% of a firm's Tier 1 capital to be classified as a Significant Risk Taker. However, this test implicitly provides for an unequal application to covered firms and, specifically, negatively impacts smaller Level 2 firms who have a lower Tier 1 capital base. It seems implausible that the regulatory agencies would purposely desire to provide larger firms with a competitive advantage; however, this non-scaled 0.5% requirement does exactly that.

-

Covered person: The proposal defines a Covered Person as any executive officer, employee, director, or principal shareholder who receives incentive compensation. There is a question of a de minimis quantum of incentive pay which would be needed to be classified as incentive compensation. For example, does a $25 spot bonus for a referral from a bank teller constitute incentive compensation? The record keeping requirement, as well as monitoring and back testing of incentive compensation plans, suggest there needs to be a threshold that, below which, the plan is not considered incentive compensation for purposes of this regulation.

-

Commission based employees: The definition of compensation, fees or benefits is a principle based definition and includes all forms of compensation. In particular, commissions would be covered under this definition. In addition, commissions would be included under the definition of Incentive-based Compensation as it serves as an incentive or reward for performance. Given there are employees who are 100% commission based, the rules need to provide clarity as it relates to the leverage maximums, e.g., 150% of a target amount. Given the volatility in fundamental business cycles, how should firms practically work to set a "target" commission amount against which the 150% maximum would apply?

-

Clawback provision: The proposal calls for a clawback feature in all incentive arrangements to allow for the recovery of up to 100% of vested incentive-based compensation from a current or former SEO or SRT for seven years following the date on which the compensation vested. The clawback would be exercised under an identified set of circumstances: misconduct that resulted in significant financial or reputational harm, fraud or intentional misrepresentation of informant used to determine the SEO's or SRT's incentive based compensation. The regulators are explicitly asking for comments regarding the time period (is it too long or too short) and whether there would be challenges that would be posed due to overlapping Federal clawback regimes.

-

Forfeiture downward adjustment period: As proposed, the forfeiture and downward adjustment process does not have an explicit time period. In theory, as proposed, a downward adjustment review could be triggered by a regulatory matter with roots in activities or behaviors that occurred ten years in the past. The regulators are explicitly asking if there should be a certain time period that should apply.

-

Equity based accounting implications: A Long Term Incentive is a plan that provides Incentive-based Compensation over a period of at least three years. Under the proposal, a Long Term Incentive plan must be eligible for downward adjustment while the awards are being earned. Given that the list of items that could trigger a downward adjustment are not formally defined, how can there be a "grant date" under ASC 718? If all material terms are not known to both parties (firm and employee) there is no grant date, and thus, there is liability accounting versus equity based accounting. This change in accounting treatment for equity compensation could result in significant quarterly fluctuations in quarterly financial results that firms must report. The commission needs to address if this was intended and the ultimate implication to a broad base of employees who receive equity-based compensation with the associated benefits of grant date accounting.

-

Acceleration only for death / disability: The proposal calls for deferrals of Qualified Incentive Compensation and Long Term Incentive compensation for a period of one to four years depending upon type of compensation and what Level a firm is classified as. During the deferral period the proposal explicitly calls for acceleration only in the event of death and disability. Thus, if there is a reduction in force where an employee is involuntarily terminated, there could be no acceleration of incentive compensation. Also, if there is a change in control, and the employee is involuntarily terminated or constructively terminated, there would be no acceleration. This proposal runs counter to common practice in both construction and also potentially afoul of individual agreements which addresses these situations.

-

Combination plans: The incentive plans at Level 1 and 2 firms are often constructed on a combination basis. For example, based upon performance in one fiscal year, an individual will receive a long term incentive plan with subsequent performance features. In this context, how would the deferral requirement work for a Level 1 or 2 firms? Does the deferral apply only after the end of the subsequent long term incentive performance period? Additionally, there is language in the proposal that suggests it is problematic to have leverage in a long term plan where the amount of the incentive is determined by the performance in the prior year - essentially requiring the employee to "re-earn" the award. The commission should address whether it was the intention to have the determination of the long-term incentive plan award be independent of prior performance.

-

Qualified performance plans: The proposal does not count as incentive compensation plans that are determined solely upon the covered person's fixed compensation and do not vary based upon one or more performance measures, e.g., a company's 401(k) plan. However, this does include by inference qualified profit sharing plans. There are important ERISA questions related to how a mandatory deferral for Senior Executive Officers or Significant Risk Takers would work within a qualified performance-based plan.

Recap: Tiering of institutional coverage

In contrast to the 2011 proposal, the current proposal categorizes covered institutions into three tiers based on balance sheet size:

-

Level 1: Firms with average total consolidated assets greater than or equal to $250 billion (subject to the most rigorous requirements).

-

Level 2: Firms with average total consolidated assets greater than or equal to $50 billion and less than $250 billion (subject to rigorous requirements).

-

Level 3: Firms with average total consolidated assets greater than or equal to $1 billion and less than $50 billion are generally subject to a basic set of disclosure requirements and prohibitions.

Important: The proposed rules reserve an institution's Federal regulator the right to require compliance with some or all of the more rigorous level 1 or 2 requirements for firms with $10 to $50 billion in total consolidated assets.

Recap: Classification of employees impacted by rules

The 2016 proposed rules indicate that all incentive eligible employees at a regulated firm are covered by regulatory guidance. This declaration requires that all incentive-based compensation arrangements must:

-

Appropriately balance risk and reward, whereby the regulators define balanced as an arrangement with both financial and non-financial performance measures, allowing for nonfinancial measures to override financial performance, and the compensation to be subject to adjustment in the event of loss, inappropriate risk taking, and compliance deficiencies

-

Be compatible with effective risk management and controls

-

Be supported by effective governance

Given that all plans must meet the requirements listed above, all broad based plans are impacted and therefore will result in the board having responsibility for providing effective oversight for plans even with diminis award amounts.

To be subject to additional requirements in the design and delivery of compensation, individuals who may have the ability to expose a firm to significant risk through their position or actions are categorized into two specific groups: Senior Executive Officers (SEO) and Significant Risk Takers (SRT).

-

An SEO is defined as a person who holds the title or performs the function (regardless of title, salary, or compensation) of one or more of the following positions: president, chief executive officer, executive chairman, chief operating officer, chief financial officer, chief investment officer, chief legal officer, chief lending officer, chief risk officer, head of a major business line, chief compliance officer, chief audit executive, chief credit officer, chief accounting officer, and other heads of a control function.

-

The definition has been expanded from the original 2011 text: "a person who holds the title or performs the function (regardless of title, salary, or compensation) of one or more of the following positions: president, chief executive officer, executive chairman, chief operating officer, chief financial officer, chief investment officer, chief legal officer, chief lending officer, chief risk officer, or head of a major business line."

-

SRTs are defined as individuals whose incentive compensation comprises at least 1/3 of total compensation and meet either of the following criteria:

-

Relative compensation test - individual is in the top 5% of highest paid (Level 1) or top 2% of highest paid (Level 2). Compensation is calculated as actual base salary paid during the calendar year plus incentive compensation awarded during the calendar year for any performance period ending in that calendar year plus with stock or options awarded during the calendar year and valued as of the date awarded. Firms have 180 days from the end of the performance year to calculate those employees falling in the top 5% or 2% of employees. It is generally expected that this relative compensation test would result in positions such as managing directors, directors, senior vice presidents, relationship and sales managers, mortgage brokers, financial advisors, and product managers to be included.

-

Exposure test - individual has the authority to commit or expose half percent or more of the capital of the institution with, for most firms, the definition of capital being common equity tier 1 capital. The rules specify exposure calculations for market risk (trading limits days of year) and credit risk (credit lending limits).

Additionally, regulators reserve the right to deem other persons as significant risk takers if they have the ability to expose the institution to material financial loss.

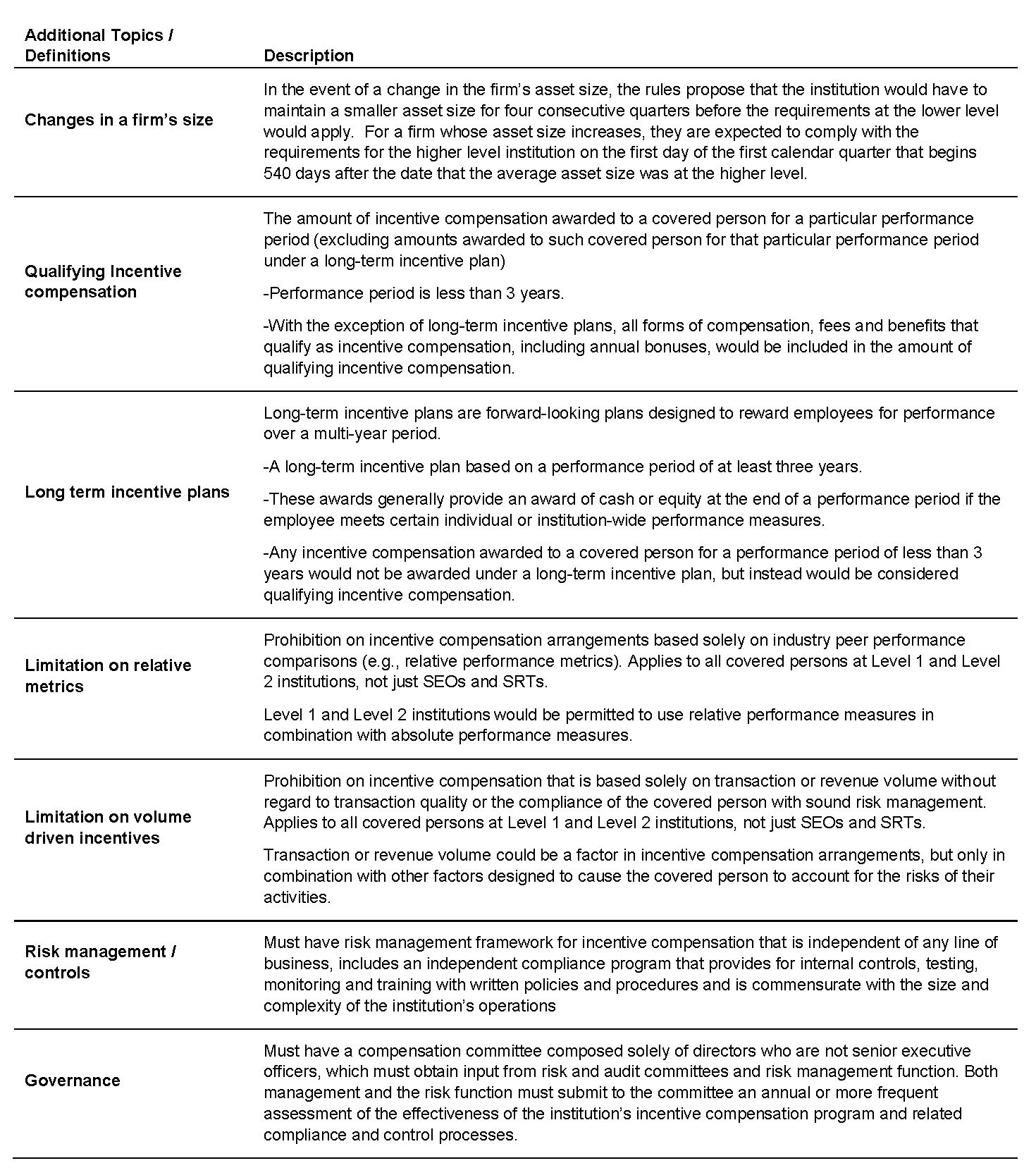

Recap: Record keeping requirements

The 2011 Proposed Rules had an annual reporting requirement that is being replaced by a 7 year record keeping requirement whereby firms must annually document incentive-based compensation structures and demonstrate compliance with regulatory rule. The record keeping required, at a minimum, would include copies of all incentive compensation plans, a list of employees subject to each plan, and a description of how the firm's compensation plans are compatible with effective risk management and controls.

Additionally, Level 1 and 2 firms would be required to maintain specific documentation of SEOs and SRTs. This documentation would include:

-

Listing of each individual listed by legal entity, job function, organizational hierarchy, and line of business.

-

Incentive compensation arrangements including deferral amounts and forms of award

-

Forfeiture and downward adjustment or clawback reviews and decisions made

-

Any material changes to the institution's incentive compensation structures or policies

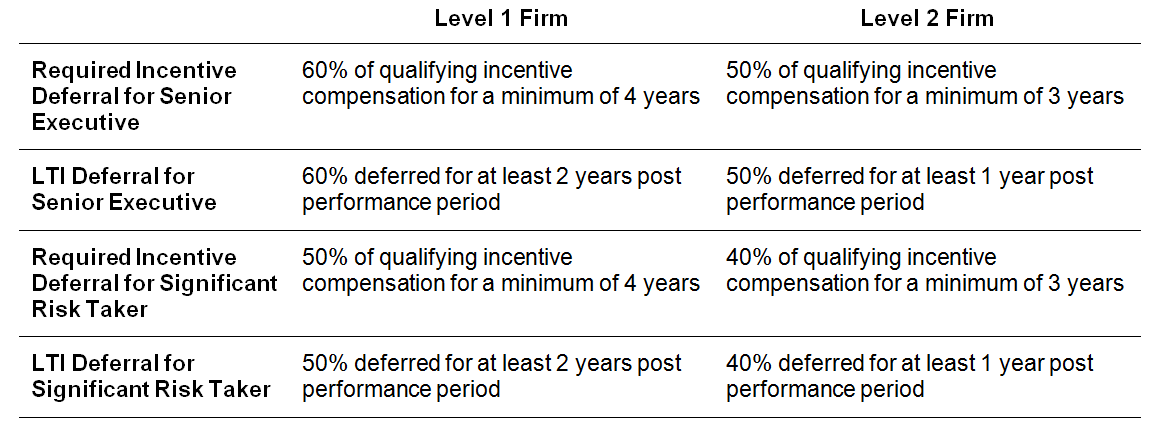

Recap: Deferral, Forfeiture/Downward Adjustments, and Clawbacks at Level 1 and 2 Firms

At Level 1 and 2 covered firms, incentive compensation must include several design features, including:

-

Deferrals: All incentive compensation is subject to a deferral as shown below. The incentive compensation while deferred must be in the form of cash and equity-like instruments and cannot vest faster than pro-rata. Note: "LTI" refers to plans having a performance period of at least three years.

-

Forfeiture: All deferred compensation, including long-term incentives, must be subject to forfeiture. The forfeiture applies to the deferral period which varies by type of compensation as highlighted below.

-

Downward adjustment: Requirements to reduce, due to various adverse outcomes (e.g., poor financial performance), for Senior Executives and Significant Risk Takers: (1) incentive compensation that has not yet been awarded during the performance period and (2) deferred incentive compensation during the deferral period.

- Clawback: All incentive-based compensation is subject to clawback for up to 7 years post vest. Given the timeframe being proposed, there could be an unintended consequence of employees significantly discounting the value of compensation delivered which could create talent retention concerns for regulated firms.

-

Stock options: To meet the rules minimum deferral requirements, stock options for Senior Executives and Significant Risk Takers cannot exceed 15% of total incentive-based compensation; this does not mean a firm cannot grant more than 15%, but anything above that amount would not count as a deferral (i.e., would further reduce the amount of immediate cash compensation awarded).

-

Leveraged capped: Maximum leverage of 125% of target pay for Senior Executive Officers and 150% for Significant Risk Takers and this limitation applies on a plan by plan basis including LTI plans.

-

Specific prohibitions defined: For firms hedging on behalf of individuals, relative performance measures in isolation, and volume-drive incentive compensation without being combined with other factors to account for risk (applies to Level 1 and 2 firms).

Recap: What has changed since the original proposal in 2011?

The Agencies issued proposed rules in 2011 and the three key principles upon which they were developed remain unchanged. These three principles state that incentive-based compensation arrangements:

-

Should appropriately balance risk and financial reward

-

Be compatible with effective risk management and control

-

Be supported by strong corporate governance

Since the initial rules were proposed, the Agencies have continued to focus their supervisory oversight on the design of incentive-based compensation for senior executives, deferral practices, including forfeiture and clawback mechanisms, governance of incentive compensation arrangements and the use of discretion, ex-ante risk adjustments, and control function participation in the design of incentives and risk evaluation. Although significant improvement has been made since the financial crisis, there are still areas where improvement needs to continue. The areas identified for continued improvement are:

-

Better targeting of performance measures and risk metrics specific to activities

-

More consistent application of risk adjustments

-

Better documentation of the compensation decision making process

Effective date of changes

The earliest date for implementation of the proposed rules would most likely be performance year 2019. This is based upon the proposal which states that the rules will apply to incentive compensation arrangements beginning the first calendar quarter following 18 months from final publication of the rules. Incentive compensation arrangements that begin prior to the effective date are grandfathered; even if they have performance periods that are completed after the effective date. The proposed rules do not affect the application of other federally regulated compensation requirements that are in effect from supervisory agencies, i.e., Sound Incentive Compensation Policies, June 2010.

Note: For a covered institution that is an investment adviser, average total consolidated assets would be determined by the investment adviser's total assets (exclusive of non-proprietary assets) shown on the balance sheet for the adviser's most recent fiscal year end. The SEC estimates that 131 broker-dealers and approximately 669 investment advisers will be covered institutions under the proposed rules. The SEC further estimates that of those 131 broker-dealers, 49 will be Level 1 or Level 2 covered institutions, and 82 will be Level 3 covered institutions and that of those 669 investment advisers, approximately 18 will be Level 1 covered institutions, approximately 21 will be Level 2 covered institutions, and approximately 630 will be Level 3 covered institutions.

Related Articles